2025 has been a turbulent year for the insurance industry. Car insurance costs are at record highs, homeowners premiums continue to climb, and regulators are stepping in to control runaway costs. These trends aren’t just numbers; they affect families’ budgets and shape decisions about coverage. In this article, we unpack the latest insurance news—from spiking auto premiums and climate-driven property risks to new rules that could ease health insurance costs. Whether you’re a driver, homeowner or health‑insurance buyer, here’s what you need to know.

Auto Insurance: Prices Soar and Claims Surge

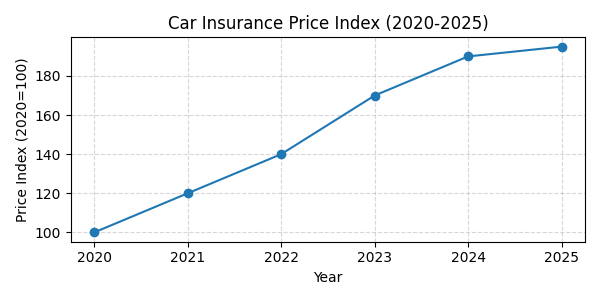

Since 2020, car insurance prices have almost doubled. Supply‑chain disruptions and an increase in natural disasters pushed claim costs up 113% in 2024, and insurers responded by hiking premiums. While 2024 marked the first profitable year for auto insurers in four years, many drivers are feeling the pinch: nearly 38% of customers surveyed said they were dissatisfied with their insurer. Insiders believe that, after several years of steep rate hikes, carriers will shift their focus in late 2025 from raising prices to retaining customers with better service. If your renewal premium seems too high, use this competition to shop around.

Homeowners Insurance and Climate Risk

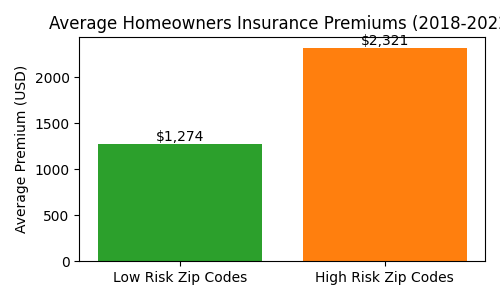

Climate change is driving huge disparities in the cost of protecting your home. Federal data show that homeowners insurance premiums are rising about 8.7% faster than inflation, and people living in high‑risk ZIP codes pay an average of \$2,321 in annual premiums – roughly 82% more than the \$1,274 paid in low‑risk areas. Insurers are also far more likely to non‑renew or cancel policies in exposed regions because the combination of more severe storms and wildfire risk is pushing claims higher. Average claim severity in high‑risk areas is around \$24,000 compared with about \$19,000 in low‑risk areas, suggesting that climate‑driven disasters are making home repairs and rebuilding far more expensive. Homeowners can reduce risk by hardening their properties and shopping for insurers that reward mitigation.

Hurricane Insurance and Storm Preparedness

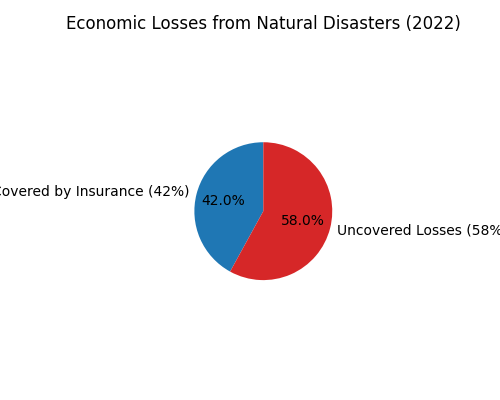

The Atlantic hurricane season serves as a stark reminder that standard homeowners policies have major gaps. Insurers generally place a moratorium on new policies once a tropical system is named, meaning you can’t add flood or windstorm coverage when a storm is already approaching. In 2022, natural disasters caused about $313 billion in economic losses and insurance only covered roughly 42% of those costs, highlighting the importance of having the right protection well before a storm forms. Homeowners in hurricane‑prone states typically need to purchase separate flood insurance (often through the National Flood Insurance Program) and, in some coastal counties, an additional wind or named‑storm policy. Deductibles for named storms are usually calculated as a percentage of your home’s insured value—often 1 to 10%—instead of a flat dollar amount. To prepare, review your coverage limits so that they reflect the full replacement cost of your home and belongings; make a detailed home inventory with photos or video; and consider mitigation measures like storm shutters or reinforced garage doors, which may earn premium discounts.

Health Insurance: New Regulations and Premium Relief

A rare bright spot in 2025 insurance news comes from the health‑care market. In June, federal regulators finalized a rule aimed at reducing premiums on the individual Affordable Care Act (ACA) exchanges by an estimated 5% for 2026. The change tackles widespread gaming of the marketplace: some brokers have been enrolling people in subsidized plans without verifying income or eligibility, driving up costs for honest consumers. Under the new rule, enrollees who report $0 income will face additional verification requirements, special enrollment periods designed to maximize agent commissions will be curtailed, open enrollment dates will be standardized across states, and insurers will be able to refuse subsidies for people not lawfully present in the U.S. (including DACA recipients). The Centers for Medicare & Medicaid Services estimates that closing these loopholes could save taxpayers up to \$12 billion next year and ease premium pressure for millions of individual-market policyholders.

| Topic | Key Numbers & Facts |

|---|---|

| Auto Insurance | Price index nearly doubled since 2020; claims costs up 113% in 2024; ~38% of drivers dissatisfied with their insurer. |

| Homeowners Insurance | Premiums in high-risk ZIPs average $2,321 vs $1,274 in low-risk areas; premium growth 8.7% faster than inflation; non-renewal rate about 80% higher; average claim severity around $24k vs $19k. |

| Natural Disasters | $313 billion in economic losses in 2022 with only 42% covered by insurance; named‑storm deductibles equal 1–10% of a home’s insured value; homeowners need separate flood and wind coverage. |

| Health Insurance | New ACA rule is projected to lower premiums by about 5% in 2026 and save taxpayers up to $12 billion; measures include income verification and closing improper enrollment loopholes. |